Should I Pay Off The Mortgage On My Home Faster? The Answer May Shock You!

How To Make Your Primary Residence An Asset In Your Real Estate Portfolio

In Today’s Issue:

🔎INSIDER INSIGHTS: Why Some Experts Say Your Home Is A Liability & Not An Asset

🤿A DEEPER DIVE: Should I Pay Off My Mortgage Faster?

📝THAT’S A WRAP: Help Us Help You!

Why Some Experts Say Your Home Is A Liability And Not An Asset

One of the best selling books of all time is “Rich Dad Poor Dad” by Robert Kyosaki.

Rich Dad Poor Dad led to a financial revolution which is a good thing.

It caused people all over the world to pay more attention to creating passive income which is definitely sound advice and why it’s such a great book.

Love The Book But I Don’t Necessarily Agree With Some Of The Implications

One of the most memorable concepts in the book is Robert Kiyosaki’s belief that your primary residence is not an asset.

In fact, he states with much conviction that your primary residence is a liability because it does not generate any cash flow. Instead it creates a perpetual outflow of cash in the form of mortgage payments, maintenance, and property taxes - just to name a few.

Consequently, many people now believe that the best course of action is to pay off their home mortgage as soon as possible. This may be a good move but is it the best move?

For our purposes, as Real Estate Collaborators serving other real estate investors, we have to be more practical and expand the context…

Three Types Of Assets

Cash Flow Assets

Examples: rental property, businesses, & dividend stocks

Equity Assets

Examples: land, cryptocurrencies, & non-dividend stocks

Hybrid Assets

Assets that have positive net equity AND positive net cash flow

could be rental property, businesses, or dividend stocks assuming that there is net positive cash flow and your equity position is greater than your financial investment

For us, our primary residence is an asset - as long as our net equity is positive and has strong to potential to keep growing.

However, we need to use leverage intelligently - the same as we do with cash flow assets (more on this topic in upcoming issues).

Inflation Defense Offense

I’d be remiss if I didn’t point out the destructive impact inflation has on the consumer’s personal economy…

Three things you need to know:

Inflation is good thing for the federal government - which is why their mandate is to keep at 2%

For consumers, inflation is destructive - which is why it’s called “the hidden tax”

Lastly, FOR YOU, the investor (Rental Property Mastery subscriber), inflation is a good thing as well

Consumers have to defend against inflation or lose by default while Investors play offense with inflation and increase the odds of winning the wealth game exponentially!

Needless to say…

You need to lay the consumer in you to rest permanently and awaken the investor inside!

And remember…

You’re an investor and using inflation to your advantage is the best way to win the wealth game!

Now to the business at hand…

Should I Pay Off My Home Mortgage? The Answer May Shock You!

I can remember more than one occasion where my wife suggested that we come up with a plan to pay off our mortgage faster, because she would feel more financially secure - especially if something were to happen to me.

Has anyone ever suggested this tactic to you? Have you suggested it to someone else? Is this part of your plan right now?

As I stated before, this tactic can definitely be a good move for anyone - but is it the BEST move for you? Only you can answer this question.

BUT WHAT IF…

Instead of paying extra money to deleverage and pay off your home mortgage faster, what if you bought a cash flow asset(s) to service the debt (make the payments) on your home.

Let’s compare the two tactics and explore which may be best for you:

David and Karen are both educators in their late fifties and, like many of us, falling short of their financial goals. Between the two of them, they have $210,000 in their retirement accounts and they just bought a new home five years ago with a current mortgage balance of $260,000 (interest rate at 5.25%) with a monthly principal and interest payment of $1,476.

They have $26,000 in savings and a positive net monthly cash flow of $1,100.

To help secure their financial future, Karen suggested that they come up with a plan to pay off their mortgage as soon as possible. However, David is friends with a Real Estate Collaborator and wants to explore the concept of acquiring income producing assets to accelerate wealth creation…

SCENARIO #1: Pay Off The Home Mortgage With Wages

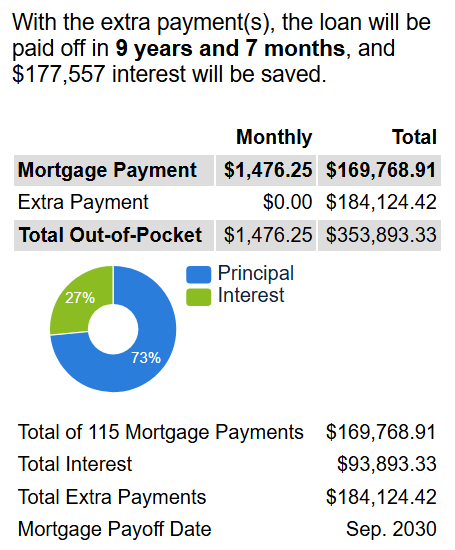

Karen used an online mortgage calculator to find out that if they used their $1,100 net monthly cash flow to make extra payments on the mortgage and withdrew $100,000 from their retirement accounts in one year (to avoid tax penalties) and added $25,000 from saving to apply toward the mortgage as well, they could have the mortage completely paid off in nine years & seven months - and save $177,557 in interest.

This strategy would allow David and Karen to eliminate their mortgage principal and interest payment ($1,476) to increase their net monthly cash flow from $1,100 to $2,576.

Assuming an average of 3% appreciation on their home, the equity in the home they bought for $275,000 in 2021 would now be $358,000 in 2031.

SCENARIO #2: Acquire Cash Flow Assets To Pay The Mortgage

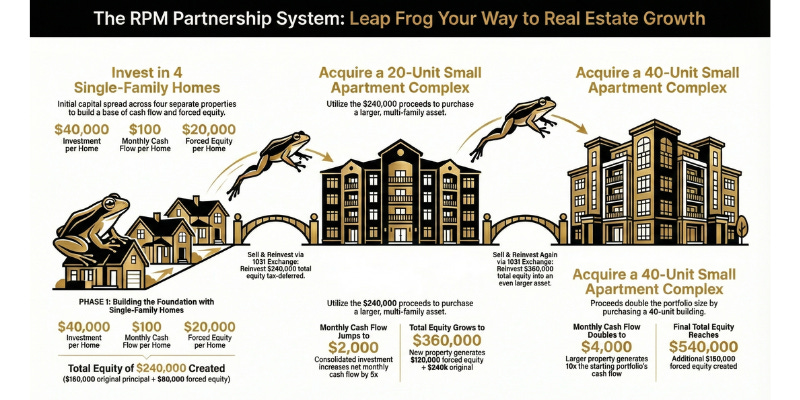

David and Karen can become Real Estate Collaborators or joint venture with one to execute a basic real estate plan like the Leap Frog Method (acquire 4 single family rentals & transition to a small apartment (recommended if you have $0 - $150K in seed capital):

This strategy would create $4,000 of passive net monthly cash flow in 6 years for David & Karen to pay the principal, interest, taxes, & insurance of $2,500 associated with their home mortgage, leaving and extra $1,500 of passive income to add to their $1,100 for a total of $2,600 of net monthly cash flow. Also, the equity created is $540,000 (not including the equity in their home).

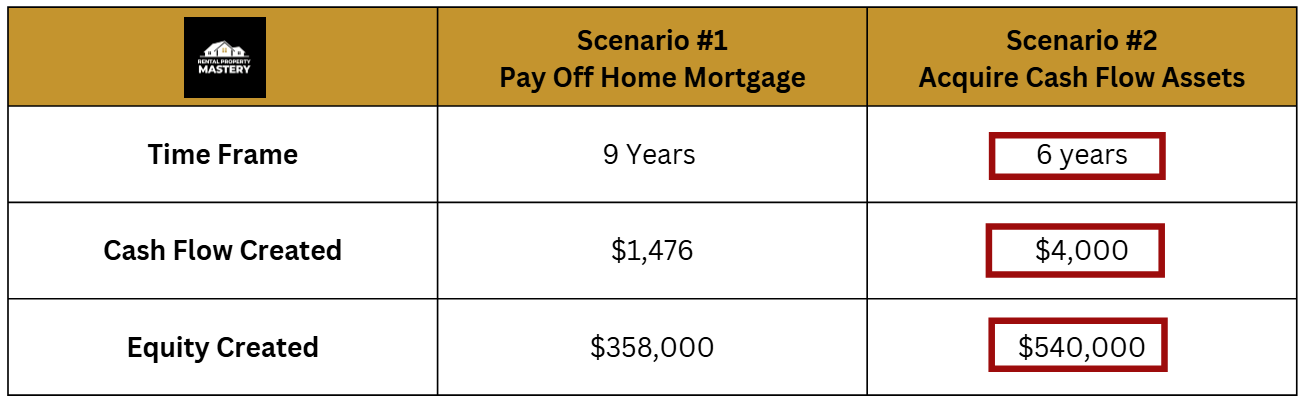

Here is the comparison:

Either tactic is good but the question still remains…

Which tactic is best for you?

Feel free to reach out with comments or questions!

Key Takeaways:

As investors (Real Estate Collaborators), we can play offense with inflation as opposed to solely playing defense as consumers

We can transform our home from a liability to an asset by looking at it from the perspective of an investor instead of a consumer

Mathematically speaking, it’s far better to have multiple appreciating assets growing our financial legacy than settling for only one appreciating asset

Passive cash flow (rent, dividends, royalties) is the ultimate goal. We create it to replace our active cash flow (wages) and win our freedom🏆

It’s never too late to create sufficient wealth for our families as long as we lay the consumer inside of us to rest permanently - and awaken the investor

Are you ready?

That’s A Wrap: Help Us Help You!

Was this useful (be brutally honest)? Have ideas on what I should publish next? Tap the poll or reply to this email. I read every response.